Overview: A market under prolonged pressure

Europe’s steel sector has navigated a series of disruptions over the past few years, marked by energy price volatility, weakened industrial output, and unpredictable geopolitical developments. According to the latest Economic and Steel Market Outlook from The European Steel Association (EUROFER), data up to the third quarter of 2024 shows that the negative cycle which began in the second half of 2022 has lingered, driving apparent steel consumption into yet another decline. Preliminary figures project a drop of around -2.3% in 2024—worse than previously estimated—before a modest rebound of +2.2% is expected in 2025.

This ongoing downturn is attributable to several factors converging at once. Stubbornly high inflation and a period of elevated interest rates have curbed investments in construction, mechanical engineering, and other key steel-using sectors. At the same time, global tensions—both in terms of energy security and political instability—have weighed on business confidence. Even as the European Central Bank started easing monetary policy in mid-2024 through gradual rate cuts, the benefits have not yet been filtered through large-scale industrial output.

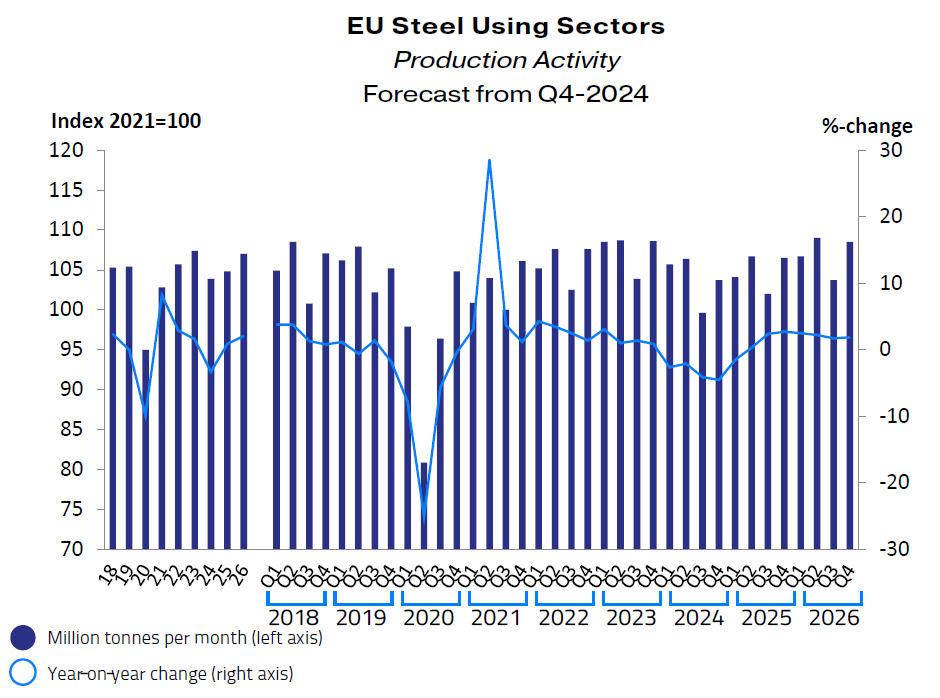

Compounding these challenges is the evolution of industrial demand. The Steel Weighted Industrial Production (SWIP) index saw three consecutive quarterly declines in 2024, mainly caused by the recession in construction (-2.2% in Q3 2024) and a sharper contraction in automotive (-12.1% in Q3). Despite the eventual tapering of energy prices from their unprecedented highs, steel producers across Europe continue to face increased volatility in operational costs, making it difficult to plan production and expansion strategies.

Data highlights (Eurofer Steel market report)

- Apparent steel consumption: -2.3% in 2024, rebound of +2.2% in 2025 (forecast).

- Steel-using sectors’ production (SWIP): forecast -3.3% in 2024, then +0.9% in 2025.

- Import penetration: around 28% share of apparent consumption, historically high.

- Industrial production: a further -2% drop expected in 2024, with a mild recovery thereafter.

These indicators confirm that European mills will continue feeling the pinch well into 2025, as real demand for steel products remains below pre-pandemic levels.

Main threats: Uncertain demand and competitive pressures

Despite the EU’s long-standing reputation for technical excellence and product quality, steelmakers must grapple with a confluence of threats:

The downward revisions in residential and commercial construction—especially in Germany, Italy, and France—signal a continued drag on steel consumption. The recent wariness toward large infrastructure projects, coupled with higher borrowing costs, has slowed the flow of new orders for structural steel, tubes, and long products. As a result, sectors like heavy machinery, household appliances, and even automotive (despite pockets of EV-related growth) have trimmed their forecasts.

Imports, including semi-finished steel, remain high in share terms (hovering around 28% of total EU apparent consumption). Major exporting countries to the EU—such as Turkey, India, South Korea, and Vietnam—continue shipping significant volumes, often with more cost-competitive pricing. Domestic producers are forced to either match these prices or cede market share, further constraining profitability.

While natural gas prices and electricity costshave partially retreated from their record highs, they still pose a risk if geopolitical flare-ups spark sudden price spikes. Additionally, decarbonization and emissions-reduction measures necessitate further capital expenditures, putting pressure on steel companies to balance short-term survival with long-term sustainability investments. Given the new impetus in Europe’s Green Deal and Carbon Border Adjustment Mechanism (CBAM), producers that lag in transitioning to low-carbon processes risk future regulatory hurdles or penalties.

With the demand still subdued, certain European mills could face underutilization, leading to structural overcapacity. This complicates investment decisions for the largest players— ACERINOX,S.A. , ArcelorMittal , Tata Steel , voestalpine , SSAB , Salzgitter AG—who may opt to consolidate or streamline specific product lines, potentially impacting local employment and supply chains.

Opportunities: Strategic modernization and value-added services

Despite the headwinds, the long-term fundamentals of the European steel sector remain compelling. Manufacturing innovations, sustainability drives, and smarter quality-control strategies offer avenues for resilience and growth.

Technological upgrades and automation: the transformation of industrial processes—often encapsulated under Industry 4.0—continues to gather pace. By investing in more efficient furnace technologies, real-time monitoring, and advanced analytics, mills can optimize resource usage and reduce environmental impacts. Adopting solutions like our Specular Vision platform can help automate surface inspection across high-speed lines, a pivotal step to ensuring zero defect targets is met with minimal human intervention.

Higher value-added steel products: in an oversupplied market, differentiation can hinge on offering specialty steels with unique mechanical or corrosion-resistant properties. Premium grades for automotive lightweighting, renewable energy structures, or advanced engineering projects consistently fetch better margins than commodity products. By combining robust R&D with modern inspection and certification, steelmakers can confidently enter these premium segments.

Digital integration and data-driven quality: synchronized data flows—linking upstream production data with final product inspection—are key to driving down scrap rates and operational costs. Through integrated machine vision solutions, producers can identify flaws in real time, segment them by root cause (e.g., raw material variance, rolling line misalignment), and initiate rapid process corrections. This approach underpins the principles of Zero-Defect Manufacturing (ZDM) and fosters accountability across the supply chain. Our Specular Vision solutions, for instance, feed data insights back into the production cycle, helping operators quickly address mechanical or temperature inconsistencies.

Sustainability as a competitive lever: despite near-term difficulties, the EU’s decarbonization agenda offers medium-to-long-term business opportunities. Mills that align swiftly with green steelmaking practices—hydrogen-based direct reduced iron (DRI) or electric arc furnaces powered by renewable energy—could secure a first-mover advantage. Many steel buyers, particularly in automotive and construction, are now prioritizing low-carbon supply chains to meet their own ESG goals. As a machine vision specialist, ISR offers targeted solutions to reduce product rework and wasted energy, thus contributing to a leaner, greener production process.

ISR’s perspective: Preparing for the next market cycle

At ISR, we work closely with Europe’s top steelmakers—Acerinox, ArcelorMittal, Salzgitter AG, SSAB, and smaller specialized producers—to adapt to a market environment that is in constant flux. Our deep familiarity with optical inspection technologies and industrial data analytics positions us to support mills through both the present slowdown and the eventual upswing.

- Advisory and Integration: We not only supply cutting-edge surface inspection systems but also offer consultative services. Our engineering teams integrate seamlessly into production lines, providing a turnkey approach that optimizes process stages from casting and rolling to final packaging.

- Customized Vision Solutions: Every steel operation is unique, with its own mechanical setups and product specs. Whether scanning for micro-cracks in high-strength automotive coils or monitoring edge defects in pipe steel, we tailor camera configurations and deep learning algorithms to deliver real-time, actionable insights.

- Cost effectiveness and ROI: In tight market conditions, capital expenditure must show swift payback. By eliminating defect repetition, saving raw materials, and reducing rework, a well-deployed machine vision system generally translates into measurable ROI within months. Plants also gain intangible benefits: stronger customer loyalty and brand reputation, both of which matter in a highly competitive global steel market.

- Scalability for the future: After a period of contraction, steel demand may gradually rebound post-2025. Firms that invest in robust, scalable inspection and quality control solutions will be poised to capitalize on fresh demand without incurring the onboarding delays that typically slow expansions.

Conclusion

Europe’s steel market continues to wrestle with multiple headwinds—demand dips, fierce import competition, and the uncertainties of a shifting economic landscape. Nevertheless, the sector’s underlying strengths and deep pool of technical expertise create pathways to recovery and innovation. As monetary conditions stabilize, we anticipate a slow climb toward more robust demand in 2025 and 2026.

From ISR’s point, prioritizing modernization, digital integration, and sustainability offers the surest road to long-term competitiveness. By leveraging advanced inspection solutions like Specular Vision, mills can reduce operational costs, differentiate their products, and lay the foundation for growth in the European market and beyond.

For more in-depth insights and to discuss how ISR can tailor our solutions to your specific requirements, please reach out through our website or connect with us on the Specular Vision Board Newsletter. Whether you are a large integrated producer or a niche specialist, let’s navigate the evolving steel landscape together and help shape a future where Europe’s steel industry remains both resilient and forward-looking.